I Personally do this: "Redeem for non-elastic lawful money by demand pursuant USCA12 section 411, signature"

I Personally do this: "Redeem for non-elastic lawful money by demand pursuant USCA12 section 411, signature"

Thank you for this, Brian.Originally Posted by Brian

Do you use this for depositing checks and/or cashing checks?

How do you sign the check?

Have you had any problems with it?

Have you had any positive results?

Does the bank where you cash your checks not require SS# or account number (if you have one at that bank)? I've noticed that often with examples people have posted here.

I haven't done any check cashing recently, but I always remembered banks requiring some sort of numeric identification when handling checks. I know my bank does for deposits, I think it would require it for cashing, too. Am I just remembering incorrectly?

Freedave, I used the phrase "redeemed lawful money" because it seems to me that your intent is that the check be credited on account as, or in the spirit of it's satisfaction having been made in "redeemed lawful money" and not simply in "lawful money" which can be construed as FEDERAL RESERVE NOTES or date entries presumed to be denominated as FEDERAL RESERVE NOTES. I felt that consistency and continuity is preserved by indicating ""redeemed lawful money" which ia a concept taken directly from the language of the legislation upon which you are depending for the purpose of effecting the libaration of the debt from "lawful money" to "redeemed lawful money". One could use the suggested phrase "non-elastic lawful money" as another suggested, but I then have to ask where that phrase is found in the subject statute. Why just shoot at the village when you have a clear scope sight line directly at the target ?

The "redemption" is effected, and somebody correct me if I am off base, by virtue of your having limited (negotiated) the terms of the check and the manner by which it is to be honored/processed under the terms of the endorsement qualifier (demand). The NOTES you receive from the ATM will be no different than any others in circulation, but the limitation is believed to be i,mposed on the bank's ability to use the fiat debt/credit capacity of the check to further their commerce of "fractional reserve banking" and debt mongering.

Now, since I believe that the banks take no notice of the stamps for the most part, and in particular when the deposit is made via ATM, I do not believe anything other than business as usual occurs in the bank when one of these qualified checks is deposited. This is why I make a photocopy of both sides of the check so to have evidence of how the check was negotiated. I am hoping that the photocopy evidence will be useful should an audit occur. We need evidence from experiences suitors relative to this supposition.

Maybe I am just off my rocker, but this matter is precisely what I hope can be cleared up by discussion and supporting facts, and that process is what I think we are engaged in presently. I also see no need for large type font or boistrous colors relative to the stamps which are being used. Everything the banks do is found as acceptable in typical fonts (some in microprinting, of which the signature line of checks is formed) and in black ink. Why come in with trumpets blaring regarding an endorsement modifier which ought to go through without a peep ?

As to the question posed about positive results, or any results for that matter; I sure would like to hear about that. Most times, we all go about doing a thing in faith without seeing proofs from those who are holding proof, or proofs against the process. Oftentimes we all go figuratively wandering in the desert and many "perish" for having used a process we thought right. So, I earnestly ask those who have had true and demonstrable benefit or damage arise as a result of using this process to please speak up and offer your proofs for our mutual benefit.

As it stands right now, it seems to me that we are acting on faith alone. I hope some suitor can prove me wrong. Please speak up and show your cards.

As for the signature; I first write "By:" and then sign it as I sign everything else; upper and lower case name as my Mom and Dad gave it to me; First, Middle and Last (as they are commonly referred to as). That is how I do it and I can give no good reason to do it that way or to do it otherwise.

Thank you again, Publius, for your willingness to address these issues.

You make some interesting points.

According to my understanding of the theory, it might be correct that the "redemption" is effected by virtue of having limited the terms of the check, but my question is, "When does the 'redemption' happen -- when the check is deposited or when currency is received by the depositor?"

Thank you also for the data on how you sign -- does anyone have any reason to do it otherwise?

The point about whether or not "we are acting on faith alone" seems to me to be very important -- have you, yourself, experienced any problems with doing this?

I join you in earnestly asking those who have had true and demonstrable benefit or damage arise as a result of using this process to please speak up and offer your proofs for our mutual benefit.

Last edited by freedave; 02-03-12 at 05:49 PM.

dave, I use this for depositing checks via the ATM, my signature card for the account was modified with "ALL transactions to be conducted in redeemed lawful money pursuant USCA12 section 411" upon opening the account which solicited some funny looks but was accepted.

I don't typically cash the checks as I don't want to solicit any ignorant questions, but all of the checks I have restrictively endorsed since last Feb have gone thru without issue.

Thank you again, Brian.

Do you withdraw money via the ATM?

And do you have any reason to believe this works beyond your own understanding of the law?

To address your questions:

Regarding when it happens. . . . I cannot show that "redemption" does actually happen. At a minimum, it seems to me that our negotiated (stated) terms are as good at a bank's negotiated (stated) terms, and our terms are expressed in the endorsement qualifier (not concealed or expressed merely by reference).

Also, it appears to our reading that the statutes which govern the Federal Reserve Bank, its NOTES; their use and function, sure does look as if "They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, District of Columbia, or at any Federal Reserve bank."

So, we made / make the damand and that is all which appears as required by the statute's stated terms for the function of redeeming. So, again, we act on faith.

Logic tells me that if an organization is given the privilege of operating under the limited capacity of a grant of government, that organization's function is likewise limited or more restricted than the powers under which the granting government functions.

I see one problem in this scenario: we, living beings, are not the depositors or account holders. We are only the signatory sureties for the named account holders, they being artifices, and ens legis, a.k.a. creatures of the STATE OF X________ (fill in the blank). The necessity of the Account holder's character as being an artifice is that the system in which it is engaged is not open to the participation of living beings. The "bank" is an artifice, dealing in artificial "money" in the character of a corporation (artificial person) under statutes and regulations (artificial law). I like to tink that their world is admiralty, of the sea; the sea being fatal to living man, a place where he cannot live. Man's place is on the nourishing land, on the shores of the sea. He may contact the sea and take from it, but never live there. We may contact the artificial world which we create and take from it (the fruits being those developed from others' contact and interaction) but we canot live in it or alter its very nature of being a hostile environment to us, the living. The accounts are named in the artificial person name and we are trying to extinguish the fiat money system which underpins the world in which the artificial persons function. Every transaction is one half money (or credit, with the transaction permanently in limbo). Artificial money cannot pay for an actual existing thing, it can only discharge the debt to another willing holder or surety. In the case of the FEDERAL RESERVE System, the NOTES and all data entries effectively denominated in notes, act as a pool of the discharged debts and place all property into a presumed limbo state wherein all property is encumbered by the entanglement of the banker's interests and claims. They get their grubby fingers on our property by getting us to label (register or otherwise restrict) the property ownership as being that of a numbered Person (individual, trust, corporation, association or other artifice.) It is a fantastic system by which most folks believe that they are protecting their assets, when in fact, they are volunteering them into bondage. SO you, living man, are only the operator of the account which is named to an artifice, and you speak for and act for the benefit of the artifice. Does that make you the trustee for the benefit of operating the account to the benefit of the artifice and its owner (the banker) ? The banker entered the artifice name on the account instead of your living being name. This was done at your directive by having provided the SSN as the primary identifier of the account.

So, I do hope that I am not on a rant here and off track. I always invite and look forward to correction. So, I believe the "redemption" happens when the qualifiedly endorsed check is accepted and processed by the bank, whether or not the process is crediting an account or exchanging NOTES.

The SSN is the hub of the wheel and the marker by which all "commerce" is recorded, regulated and taxed.

Question #2 asked about problems. I have had no problems relative to this process, but neither can I claim any benefit.

Publius commented:

We need evidence from experiences suitors relative to this supposition.

We have plenty of evidence but there is an element that prevents enough details for a proof over cyberspace. A comprehensive evidence package is not available. There are suitors who are tax preparers and even bankers/licensed tax preparers but they like to filter their experiences sanitized, even with other suitors. If a suitor broadcasts details, fine; that is why we call it a brain trust. We trust each other. If a suitor sends something interesting to me though, I will sanitize it and broadcast it with my commentary. If it is a success story about the IRS though, I will send the sanitized rendition and comment back to the suitor alone for approval before I broadcast it to the brain trust.

We do not have a lot of sanitized success stories because I just do not bother with the sanitizing process unless a better example comes along and since they are sanitized, they cannot be verified and you will just have to believe me... So it gets so no better success stories come along until somebody is willing to give their address and SSN over the Internet.

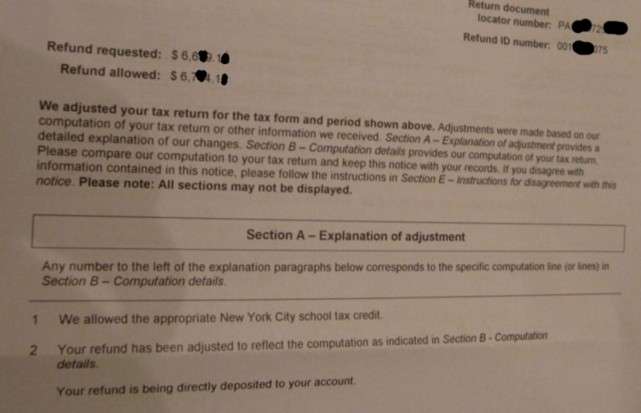

One of my favorites is this one where NY (METRO's Finest) pondered the state tax return carefully enough to add on the $125 School Tax Credit but did not flag that there are thousands of $$$ of withholdings on zero taxable income!

If you want to look at those figures awhile, you might be able to convince yourself I am not lying.

However on Quatloos I am moderated and forbidden to show examples like this because, If you are going to show examples boasting that you can break the law, they have to be verifiable!

I worked carefully with the suitor and have shown you exactly what he is comfortable with me showing you.

Last edited by David Merrill; 02-05-12 at 12:48 AM.

Thank you again Publius.

I looks to me like much of what you wrote may derive from the redemption/commerce ideas of people like Winston Shrout, Tim Turner, etc., which I do not understand very well and the results of which I have not been able to verify.

How long have you been attempting to redeem lawful money in terms of how many checks you have deposited, how many checks you have "cashed"?

Reply With Quote

Reply With Quote