That's an interesting statement that I have never seen stated before.Originally Posted by NYGMan-Tax

I have never heard of the IRS collecting a value tax.

I thought the IRS collects income tax?

That's an interesting statement that I have never seen stated before.

I have never heard of the IRS collecting a value tax.

I thought the IRS collects income tax?

Treefarmer

There is power in the blood of Jesus

Assuming, as David Merrill does, that you are genuine in your inquest, let us delve into your opinions further:

As to your "point 1", I believe David Merrill has answered that sufficiently and proficiently citing the code, and relevant cases, relating to the issue. However, one little word may be the cause of confusion:

It is, "They shall be redeemed in lawful money on demand..." rather than your "point 1" which reads, "You can redeem FRN's for Lawful money". That may be an overlooked distinction but I believe it makes a difference. FRNs redeemed in lawful money suggests that the very same paper functions as lawful money if the demand is made on the record. It makes no difference that the paper "appears" the same to the eye; that paper is now redeemed and the remedy from the fees/tax associated with endorsing elastic currency and credit exists between your ears and is extant pursuant to the law.

So your potential obfuscation by using the word "for" rather than "in" is refuted for cause.

Your next point, which you feel is "more problematic", is that anything of value is taxable. While that may be true for most, that truth is based on the presumption that whoever acquires "anything of value" is a voluntary signature endorser of the elastic currency and credit of the Federal Reserve thereby creating a tax burden on anything of value obtained by way of said signature endorsement.

The premise and presumption of voluntary participation with the FED's system of false balances is why you posit "anything of value is taxable". So in that regard you are correct; whether you recieve eggs, cars, furniture, clothes, gold, silver, pesos, etc., if one consents or acquiesces to the presumed notion that one is a willing participant in the FED's credit and currency system, than there is a tax burden associated with "anything of value".

That tax burden of "anything of value" would be considered compelled servitude/slavery if not for the extant and required written-in remedy in the law found at Title 12 U.S.C. ?411. That remedy relieves culpability of debt-enslavement since participation and endorsement is voluntary. One simply can make one's demand clear and on the record of one's intent and desire to be set apart from the abomination of false balances and the chattelization of human flesh and bone as the surety-bond substance behind the elasticity of the FED's currency and credit.

Wow, Anthony Joseph, that was a very well thought out response. It was the best one I've read about how redeeming lawful money gives remedy against servitude. Thanks. I understand it better now.

You are quite welcome.

The most important part of this issue is getting "remedy between your ears" and forming the record. This does not, however, guarantee you will be without strife or not be subject to further "tests" of your conviction. The truth does have power but it is God Almighty who decides how the truth will manifest for each of us. So there may be some who heard the truth and acted upon the truth but yet felt somehow "it didn't work". We have to remember it is not for us to decide if it "worked", it is our desire to seek and act upon the truth even though we may think "it didn't work" out of our lack of understanding or knowledge of God's Will.

The record is clear and it is ultimately God who judges the record. He will decide the manifestation and outcome of our actions and the actions of others. All we can do is act in honor, truth and peace as best we can and pray that He will lead us upon the righteous path regardless of our potential misguided notions of failure.

I find that part to be most challenging for me, keeping my thoughts and faith in check in the face of what sometimes seems like total ignorance, disregard and dismissiveness from those who are with the charge of administering and guarding the Kingdom - IN GOD WE TRUST and SO HELP ME GOD.

That is all very well put Anthony Joseph. I want to describe that trust system (fiat currency) a little better for the readers.

The IN GOD WE TRUST trust began in 1863.

The SO HELP ME GOD is the swearing in of public officials - a fungible fidelity bond:United States currency has the inscription “In God We Trust” in a place the Secretary decides is appropriate.

I am not getting it, it still doesn't work. there is inherent value in what you are getting from a second party. What ever the form of the value received, it is taxable. the fact that you don't consider it valid currency is irrelevant. I get paid in USD, EURO, British Pounds, Canadian Dollars, to name a few. I have also been paid in property for my services. Under all scenarios, the money I was paid, regardless of denomination and form is taxable.

I am just getting a bit frustrated with the lack of authority for this position. I can't find an IRS code section, regulation, or case to support this position. I know you all believe this opinion, and in David, but unless supported by the tax laws, it just doesn't work. David could apply for a PLR present his position to the IRS, and have them rule on it. At least with that the IRS would provide their logic and analysis. The only issue is the IRS will not opine if they believe the argument is not frivolous, and based on some of the case law I have read, that may actually be the case.

NYGMan-Tax, it is indeed a pleasure to have you here.

You bring a new perspective to this discussion forum.

Thank you for joining us.

Earlier today I dug out my searchable copy of the 1986 IRC and searched for the term "value".

"Value" occurs there 3,416,179 times, usually in connection with "interest" or "estate".

Then I searched for "value tax", which occurs not at all, and neither does "taxable value", "tax value" or "inherent value".

Then I searched for "tax on value", which occurs once:

----------------------------------------------------------------------------------------------------

Subtitle F - Procedure and Administration

CHAPTER 62 - TIME AND PLACE FOR PAYING TAX

Subchapter B - Extensions of Time for Payment

-HEAD-

Sec. 6163. Extension of time for payment of estate tax on value of

reversionary or remainder interest in property

-STATUTE-

(a) Extension permitted

If the value of a reversionary or remainder interest in property

is included under chapter 11 in the value of the gross estate, the

payment of the part of the tax under chapter 11 attributable to

such interest may, at the election of the executor, be postponed

until 6 months after the termination of the precedent interest or

interests in the property, under such regulations as the Secretary

may prescribe.

-----------------------------------------------------------------------------------------------------

I find it interesting that you stated that anything of value being received is taxable by the IRS.

Perhaps value is not taxable under the IRC, but pursuant to public policy?

Would you please elaborate on your statements about value being taxable?

Thank you.

As to your curious statement about someone not considering "value received" as "valid currency", this really caught my eye.

You did not appear to be addressing anyone in particular with your statement, so I assume that you were directing your comment at the collective forum members.

A quick forum search revealed that we have never discussed the validity of any currency on this forum, and the word combination of "valid currency" exists exactly once on this forum in your own post.

So while you are at it, would you please also explain how "received value" is "valid currency"?

Thank you, your input here is appreciated.

Last edited by Treefarmer; 10-19-12 at 02:30 AM.

Treefarmer

There is power in the blood of Jesus

It will take some time to go through your flurry of posts but again, I address the juxtaposition of premise with your initial sentence.I am not getting it, it still doesn't work. there is inherent value in what you are getting from a second party.

There are 'boxes' in which we are conditioned to think and Treefarmer has already presented an excellent item for another reality check:

So just to get our heads out of a certain box that you propose to draw consider the sales tax. Sales tax is a burden on the shopkeeper, not the buyer. It would be a buyer's tax if it was intended for the purchaser. It is such an ingrained tradition though, that people are accustomed to paying the sales tax for the shop owner. The shopkeeper should subscribe to the letter of the law and just put the sales tax into the purchase price, in an OCD world, don't you think?I have never heard of the IRS collecting a value tax.

Importing the principle of your 843 Form rebuttal I read yesterday you do not seem capable of seeing over the edge of the teacup and think that is the scope of the horizon here. All you need to do is figure that the Income Tax is a fee on the use of the Fed's private credit. Then you might understand much better how redeeming lawful money by demand (by making your demand) removes the suitor into the still extant currency realm of US notes and coins.

Regards,

David Merrill.

P.S. Your myopia is supported by the facts:

Prove I am "under the code":

NYGman says;

That is not proof.

Yet we have been redeeming lawful money in various forms for seven years now.

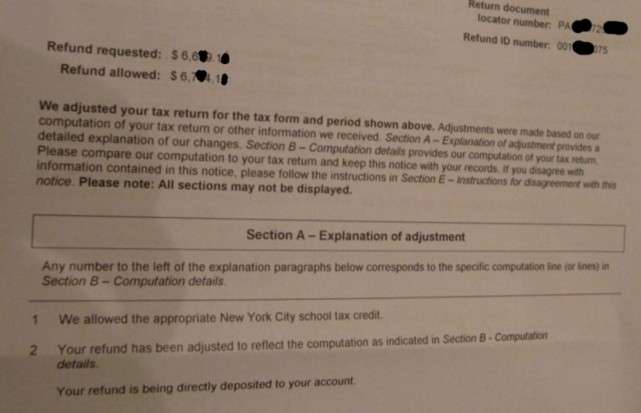

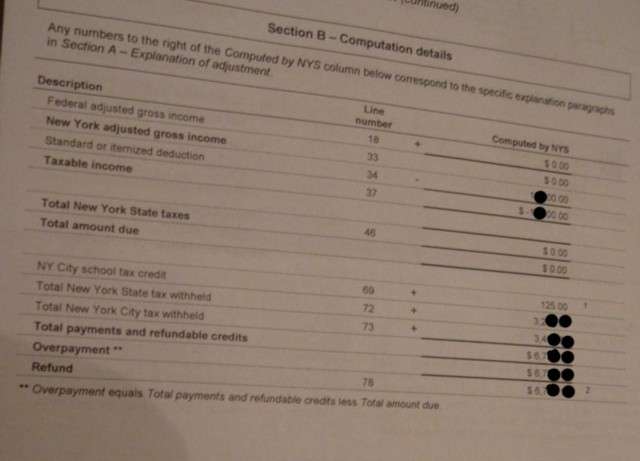

That snippet is from my current emails. You will get no proof over the Internet. My favorite examples show contemplation like that though - that the IRS considered it carefully and then cut the check, even to apply it to back taxes. Or closer to home (yours) would be the state tax authority pondering over a tax refund carefully enough to add the School Tax Credit on:BTW: I just got my State refund check (over $3,000) , based on the 1040 Line 21 "Lawful Money Demand Reduction". The Federal refund was already successfully applied to back taxes. The other State tax return was also accepted without objection to this reduction. So, "...by the mouth of 2 or 3 witnesses, a matter is confirmed"! Hooray!

You have a good point. The recipient in New York is a banker for the huge international bank and is a licensed tax preparer. He was at a get together and overheard his co-worker's (the host's) sister, an IRS attorney speaking a bit too candidly, There is a group of people in Colorado who don't pay Income Tax; they are doing it correctly. He figured she meant me but she clammed up to any further conversation about it. She would however speak a little about his returns and at one point, the next year she remarked that she could no longer access his files.

This sort of thing goes on around me all the time. It is not proof to you because like you see, I bounced it back and forth with him until he was comfortable that nobody would figure it was him. But even if you do, what are you going to do? Are you going to call up the NY Tax Authority and gripe about somebody else getting a refund? You would be griping to the people who write the refund check! You would call them up and tell them they made a big mistake?

So we discussed it carefully and found these two docs as sanitized are convincing that they go together and they show contemplation. As you read it, it is not proof - agreed. But you have to admit it is rather convincing.

Regards,

David Merrill.

Posting Permissions

Posting Permissions

Reply With Quote

Reply With Quote