-

Administrator

The signature card is an agreement. You make a novation (innovation) and that means they have three days to R4C your novation. Another method might be to put the demand on your payroll authorization for direct deposit. That involves your employer though and that is never wise.

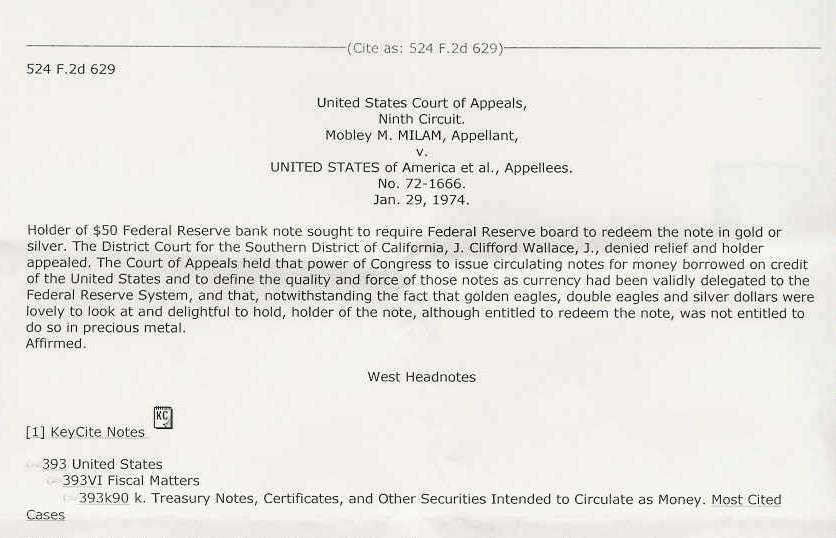

I think you are right on about the specifications of which banks may be redeemed but you do not get to bank at the Federal Reserve banks. They do not open accounts for people like you. So you either have the right to redeem or not. According to MILAM you do.

Which presents the question - Where do I go, if not my bank?

If your banker says you have to go to the Fed or that this only applies to state banks and not you and if he were correct then it would not make any difference and he should allow you to sign as you please. If you have no such remedy then it is just a fanciful addition - meaningless. We have the suitor who found employees being fired though, for making general deposits when they were to be special deposits to it does indeed matter.

My experience (through the brain trust) tells me that if the suitor knows what he is doing he will get the novation in place mostly because the bank has fiduciary responsibility to do business with you. In other words they may try convincing you to close down your account and if you are conditioned to obey, you will. They will not close down your account unless you are costing them like with the suitor where the employees were fired. That cost a lot so they shut down the accounts.

Last edited by David Merrill; 01-12-13 at 08:37 PM.

Posting Permissions

Posting Permissions

- You may not post new threads

- You may not post replies

- You may not post attachments

- You may not edit your posts

-

Forum Rules

Reply With Quote

Reply With Quote