Greetings, all.

David, and all in general,

I and many others have been experiencing resistance or downright refusals to change our signature card or open new accounts as such with a declaration that the account be redeemable in lawful money. I have a theory but I do not have proof one way or the other why these 'member banks' have been rejecting us.

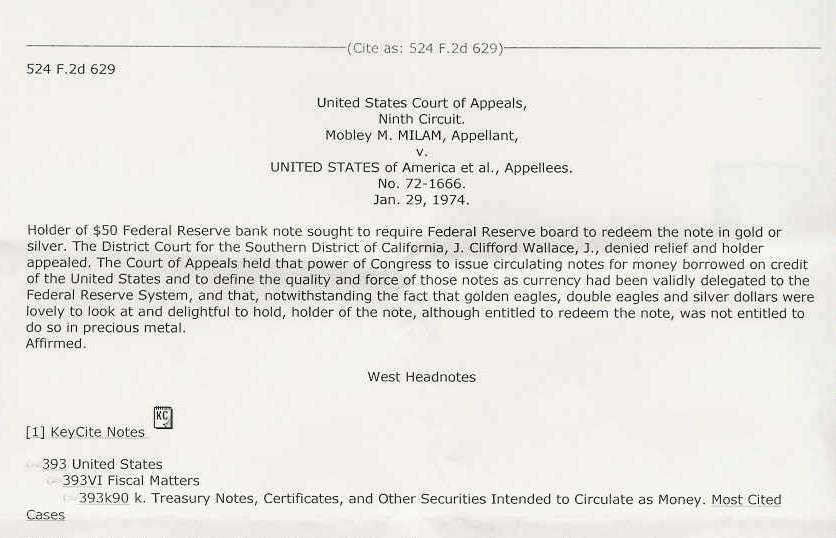

USC 411 states that 'The said notes shall be obligations of the Unites States and shall be receivable by all national and member banks and Federal Reserve Banks...They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, DC, or at any Federal Reserve Bank.'

Here goes my theory based on the language in USC 411...

1) 'The said notes...shall be receivable by all [banks]'.

To me, receivable means they can accept Federal Reserve notes (with no talk of lawful money redemption at this point). So they can receive FRN's into virtually all banks.

2) 'They shall be redeemed in lawful money on demand at the [Treasury Dept, DC, or any Federal Reserve bank].

What strikes me is that 'member banks' are not included in the 'redeemable entity' list. The language could be interpreted in this manner by the 'member banks': any bank can receive FRN's into an account, but only the ones in the 'redeemable entity' list shall as obligated by law, redeem them in lawful money. So they are interpreting 'Federal Reserve bank' to mean the 12 known banks as such. Therefore, they (private, FDIC members, that ilk) interpret that they can receive your FRN's but are under no obligation to redeem in lawful money because they are not one of the '12 Federal Reserve banks'.

Although remedy exists via USC 411, the thinking is that if these 'member banks' are somehow excluded from the obligation, one would need to redeem in lawful money at one of the 12 Federal Reserve Banks or at the Treasury Department. Which for almost all of us would be incredibly impractical and frankly, incredibly unfair and not in good faith per USC 411.

Is there supporting law or documents for USC 411 that would clarify the above interpretation one way or another?

Thank you for any clarification or thoughts on this.

David, and all in general,

I and many others have been experiencing resistance or downright refusals to change our signature card or open new accounts as such with a declaration that the account be redeemable in lawful money. I have a theory but I do not have proof one way or the other why these 'member banks' have been rejecting us.

USC 411 states that 'The said notes shall be obligations of the Unites States and shall be receivable by all national and member banks and Federal Reserve Banks...They shall be redeemed in lawful money on demand at the Treasury Department of the United States, in the city of Washington, DC, or at any Federal Reserve Bank.'

Here goes my theory based on the language in USC 411...

1) 'The said notes...shall be receivable by all [banks]'.

To me, receivable means they can accept Federal Reserve notes (with no talk of lawful money redemption at this point). So they can receive FRN's into virtually all banks.

2) 'They shall be redeemed in lawful money on demand at the [Treasury Dept, DC, or any Federal Reserve bank].

What strikes me is that 'member banks' are not included in the 'redeemable entity' list. The language could be interpreted in this manner by the 'member banks': any bank can receive FRN's into an account, but only the ones in the 'redeemable entity' list shall as obligated by law, redeem them in lawful money. So they are interpreting 'Federal Reserve bank' to mean the 12 known banks as such. Therefore, they (private, FDIC members, that ilk) interpret that they can receive your FRN's but are under no obligation to redeem in lawful money because they are not one of the '12 Federal Reserve banks'.

Although remedy exists via USC 411, the thinking is that if these 'member banks' are somehow excluded from the obligation, one would need to redeem in lawful money at one of the 12 Federal Reserve Banks or at the Treasury Department. Which for almost all of us would be incredibly impractical and frankly, incredibly unfair and not in good faith per USC 411.

Is there supporting law or documents for USC 411 that would clarify the above interpretation one way or another?

Thank you for any clarification or thoughts on this.

Comment