Are you paying attention? What I am bringing to attention here are fundamental theories and techniques behind psychological operations, psychopolitics (same thing?), marketing, persuasion and the like--even to attitude change on a political or societal level. We've heard of "mind control" and so on but how many of us have actually looked into the academic theories and details behind it all? Isn't it interesting how much thought has gone into not only how you think but how to change your mind --and if not yours the minds of others to accept something or another?

The Elaboration Likelihood Model (source: Wikipedia)

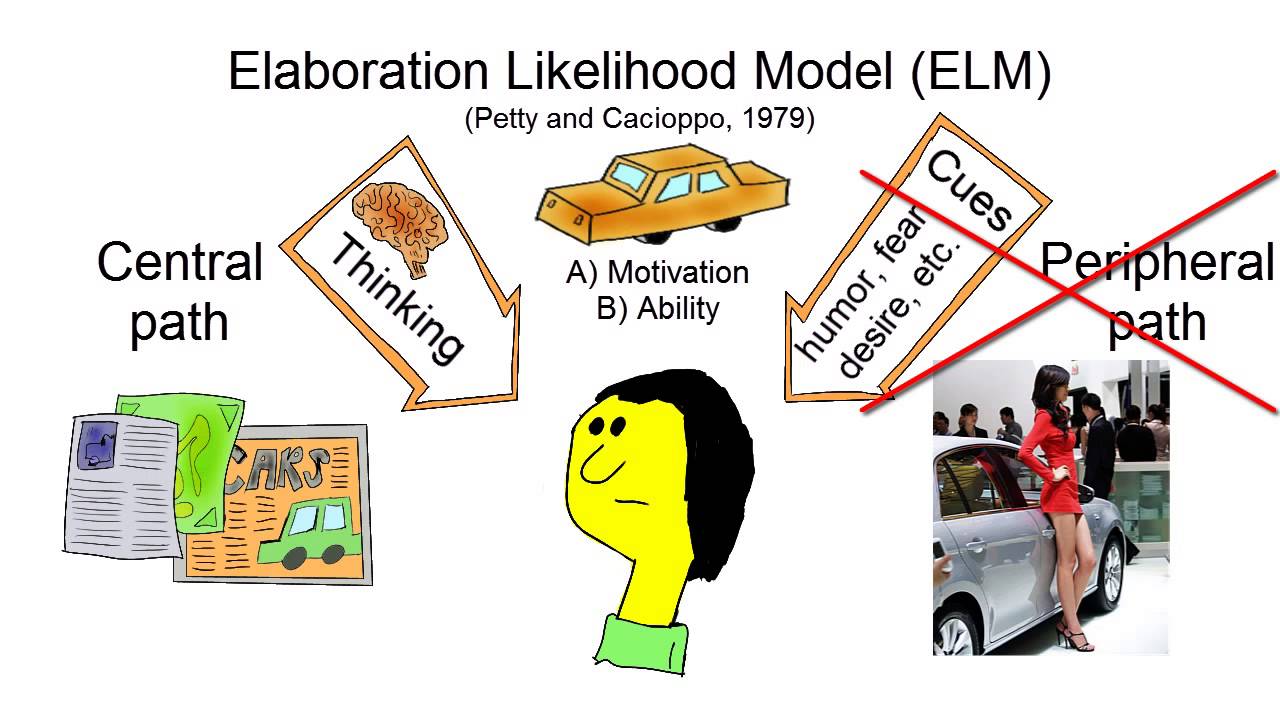

The elaboration likelihood model (ELM) of persuasion[1] is a dual process theory of how attitudes are formed and changed, which was developed by Richard E. Petty and John Cacioppo during the early 1980s. The model examines how an argument's position on the "elaboration continuum", from processing and evaluating (high elaboration) to peripheral issues such as source expertise or attractiveness (low elaboration), shapes its persuasiveness. ELM resembles the heuristic-systematic model of information processing developed about the same time by Shelly Chaiken.

The elaboration likelihood model (ELM) of persuasion[1] is a dual process theory of how attitudes are formed and changed, which was developed by Richard E. Petty and John Cacioppo during the early 1980s. The model examines how an argument's position on the "elaboration continuum", from processing and evaluating (high elaboration) to peripheral issues such as source expertise or attractiveness (low elaboration), shapes its persuasiveness. ELM resembles the heuristic-systematic model of information processing developed about the same time by Shelly Chaiken.

(*) The Elaboration Likelihood Model of Persuasion (PDF), Richard E. Pettty, John T. Cacioppo;

(*) Seven Models of Framing: Implications for Public Relations;

(*) Social Judgment Theory.

How might the above have been used to sell scrip over gold/silver specie over lawful money? How might the above have been used to push the Federal Reserve Act?

Comment