-

-

Thank you for registering. It is great that you have educated yourself about the right to redeem lawful money instead of endorsing private credit from the Fed before you began execution.

It is refreshing that you are confident enough to feel giggling inside rather than the traditional emotional suppression caused by thug-like behavior from allegedly civilized bank officers. Your post reflects a protectionism, not ignorance. Those officers knew you have this right yet they tried to stare you down with cold hatred. I consider these posts to be stepping stones toward a goal; intelligence reports. Your report tells me that the banking cartels of the world have suffered a major loss with your non-endorsement of private credit.

And at Bank of America at that! -

Question:

Is lawful money reserve currency that banks use to underwrite their fractional reserve lending?Comment

-

I believe the Answer is more fundamental than that Question begs.

If you have ever watched Gary FIELDER's The Gig is Up then you might better understand how much money is being circulated electronically that never comes into actual creation. This is something I call electronic vaults. The first "banker" ever, who issued more script than he had vaulted value is still unjustified. The Fed Act might be considered an interlocutory appeal, meaning that endorsers post the bond that keeps that banker and every banker after him who has engaged in fractional lending from jail on a supersedeas bond.

They are all convicted by the facts; they just keep the sentencing from being executed by posting a bond during appeal.Comment

-

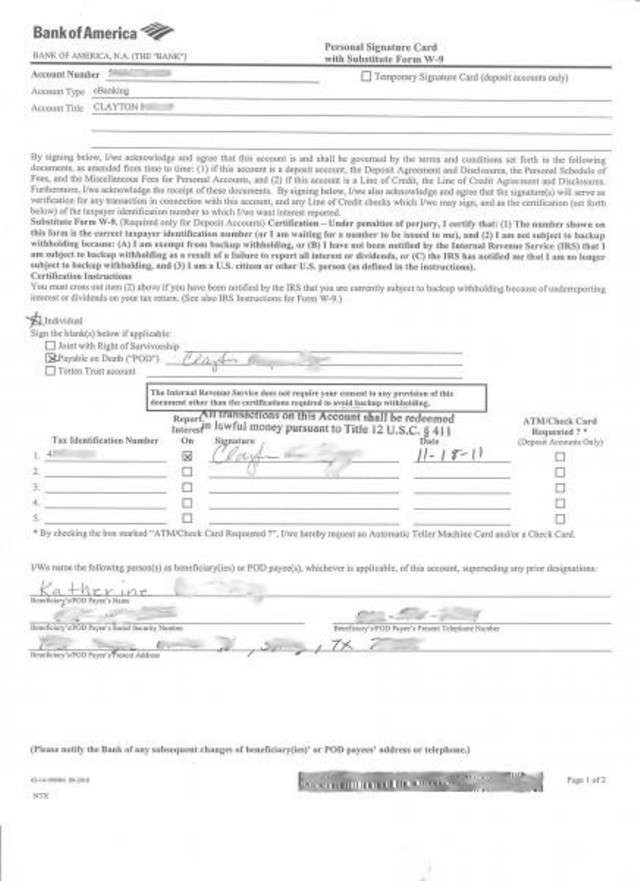

BofA Deposit Account Signature Card

Today I opened a BofA deposit account to have my payroll check direct deposited. My wife opened a separate deposit account as well. When it came time to sign the signature card my wife pulled out our lawful money stamp from her purse. I stamped my signature card then autographed the card. My wife stamped her signature card upside down. The clerk offered to re-print the signature card so she could re-stamp it correctly. Of course the clerk had no idea what the stamp was about. After we finished I asked for her to make copies of the signature cards for us. After she made the copies we noticed she carried them over to the bank manager. Soon the clerk returned, handed us our papers and politely asked what was the stamp about. She said her bank manager did not understand the purpose of the stamp either. My response was that it is for tax purposes. Attached FilesFishnet

Attached FilesFishnetComment

-

-

Again, it is quite refreshing to see such clear demonstration that remedy can be easily understood and executed. I receive your remedy in place as a compliment to my communication skills, considering that you are not a suitor. You have received this website as a lesson plan and are discovering the power of the law in execution.

Wonderful! Thank you for sharing with us.

P.S. I expanded the image above a little but would like for you to give us better resolution please:

Last edited by David Merrill; 11-19-11, 09:38 AM.

Last edited by David Merrill; 11-19-11, 09:38 AM.Comment

-

What did your lawful money look like, can you scan a copy?"And if I could I surely would Stand on the rock that Moses stood"Comment

-

Lawful money appears as one and the same as Federal Reserve Notes. As David has quoted the Federal Reserve website, and as the Treasury.gov website states "United States notes serve no function that is not already adequately served by Federal Reserve notes. As a result, the Treasury Department stopped issuing United States notes, and none have been placed into circulation since January 21, 1971."Originally posted by Chex View Post

The point being that you make your demand via restricted endorsement on the back of the check and/or via the signature card on the bank account. Once your demand is known for that specific instrument, you have lawful money in hand. As David states, do not worry what the bank does behind the counter, you will get wrapped around the axle of the banks problem. It is not your problem. You have completed your requirement by making your demand.Attached FilesLast edited by fishnet; 11-19-11, 04:01 PM.FishnetComment

-

-

A very basic lesson I learned over the past few years; Know who you are. Have no fear of success or failure.Originally posted by David Merrill View Post

I am a man created in the image of the Creator. I have an inheritance from the Creator; Dominion over all earth and everything upon it, including creations of man. Most people (not men) are fearful of success and of failure because they lack confidence in themselves. Knowing who you are restores that confidence that was taken from you as a child through conditioning.Last edited by fishnet; 11-20-11, 05:26 AM.FishnetComment

-

Originally posted by fishnet View Post

Yes, a unique expression of God, in His image.

I have been executing some exercises in that same direction myself. Convert fear to love. Deny the fear, not the danger. You can deal with the danger much more appropriately if you have love in your heart instead of fear.

When you frighten people into being threatening like at your bank; you are definitely in danger. Handling the situation without fear though, you walked through the danger unscathed and with your objective (remedy) accomplished. Admirable!Comment

-

I too have encountered this type of hassle at several different banks; and I comprehend that a check is an instrument of the bank ordering the bank to pay the payee. Is there a statute in the USC or UCC that states this fact clearly so that it can be brought up in conversation when the teller refuses to execute the the order without a fee?Originally posted by fishnet View Post

I have tried finding something solid to back this up and have only found information to the contrary. Such as,

Question: Can a bank charge a check cashing fee to non-customers?

Answer: Yes. Institutions are allowed to charge a check cashing fee. The Department issued a press release on August 31, 2001 regarding this matter. Since then, the court ruled that the Texas law was not enforceable and therefore the institutions could continue the practice of charging a fee for cashing their checks.

source:http://www.dob.texas.gov/exec/faq.htm

I'm not doubting that the bank is required to cash their instrument, I'm just looking for a way to prove it to them.Comment

-

I figure that the law really reads that if they have notified you they will be charging the fee, they can. Notice and grace; that is the law. When you are there at the counter though, they have to cash the check and cannot charge you. What I mean is the law of "next time" prevails. When I was experimenting (vicariously through suitors) we encountered this "next time" law consistently. One suitor went three times and always got a "next time" to his objections.Originally posted by christopher george View Post

That is what the law is in my opinion and I believe it is coherent with the UCC in many sections. You have to make the Notice CONSPICUOUS and if you just showed up there to see that there is a sign saying, IF YOU DO NOT HAVE AN ACCOUNT WITH US WE WILL CHARGE YOU $5 TO CASH A PAYCHECK, that does not cut it for notice. Maybe they will rag on you about, Last time we told you next time.

The enforcement is your boss. When we were toying with this in the brain trust the ammo was, I don't think my boss intended you to have $5 out of my pay. Pushing that would be, Please call the CFO where I work and see if he wants to pay you $5 to cash my paycheck or would rather move the account to another bank.

Thinking over this post, I beleive I have described banking law quite well. I believe I could pretty well guarantee that you will walk out of the bank with your $5. The Law of Next Time of course includes your own notice and grace. When they tell you next time there will be a $5 fee you counter:

Oh, no you don't! Next time you will not be charging me a fee too.

Regards,

David Merrill.Last edited by David Merrill; 01-16-12, 10:46 PM.Comment

-

Very informative post! Regarding BofA, it is good opportunity to review the best credit card offer and see which if any make sense for you. Most charge card rewards programs pay card holders for spending and adding to debt. However, Bank of America recently released a new card that rewards people for paying off debt. The BankAmericard Better Balance Rewards card incentivizes consumers for paying their regular bills on time and for throwing in a little more over their minimum charge.Comment

-

Most who redeem lawful money will use only debit cards - for convenience of plastic and Internet transactions.Comment

-

I'm really starting to get the notion that these excessive fees and such amount to a private tax. If the check is drawn on the bank and they are out to charge a fee to cash the check, that seems like a kind of unfair trade practice or a breech of trust. Some people might be astonished at the idea of banks having for the past 30 years or maybe more instead of existing to make it easier for folks to do transactions have pretty much gotten in the way. Like a bunch of Medieval tyrants blocking the way to an amusement park just because they can. For example, some bank's wont activate Wire Transfer. They dont tell you much at all about the services they offer. They do many things to impede. Some banks will block Fedwire transactions altogether. Some will refuse checks. But has seemed they've always been out to charge more fees for doing less of anything useful to the 'customer'. Some even charge a fee for calling customer service!

This obstinate bullheaded silliness has extended even to property managers who seem to think debit cards or credit cards are the only two sensible payment methods even for $3,000/month apartment leases. If a customer asks them their bank account so they can wire the payment they decline "Oh we can't give you that information". But yet they probably know the renter's SSN, DOB, high school of graduation, all employment information, bank name, bank account number, where they live (obviously), what car they drive, their license number, names of all of their children. What the ... ?

Why anyone would tolerate that kind of crap, I have no idea.

Same for car dealerships. Right from the start and without any transaction pending or guarantee that you'll get any car they want to lift your driver license and gather information about you. Turn around and ask them for their sales tax number, the state charter number, the exact legal name other than what's on the slick sign outside and you might gather gazes like you were Bruce Lee standing next to two lesbians holding hands at a KKK rally--even though almost every single English jurisdiction probably requires them to hang the information on the wall in a conspicuous place. That you are interested in identifying them specifically seems to be "offensive" to them as if by doing so you would be thwarting some kind of trickery. WHY EVER WOULD ANYONE TOLERATE THESE KINDS OF THINGS?

So here consider private tax through inconspicuous private notice but yet they conceal the information they are supposed to make conspicuous? Hmm.

It might be actionable under RICO that banks are attempting to strongarm money out of folks simply for having banks honor demands against them per customary commercial law. Seems like racketeering. If the check is drawn on BoA (constrictor?) remember BoA isn't a third party check cashing service then.Last edited by allodial; 08-21-14, 04:57 PM.All rights reserved. Without prejudice. No liability assumed. No value assured.

"The object in life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane." -- Marcus Aurelius"It is the glory of God to conceal a thing: but the honour of kings is to search out a matter." Proverbs 25:2Prove all things; hold fast that which is good. Thess. 5:21.Comment

- If this is your first visit, be sure to check out the FAQ by clicking the link above. You may have to register before you can post: click the register link above to proceed. To start viewing messages, select the forum that you want to visit from the selection below. If you would like to post in these forums please send a PM directly to David Merrill.

- All transactions on PayPal and elsewhere are demanded to be redeemed in lawful money as found in Section 16 of the Fed Act and at Title 12 USC 411.

- Thank you so much for enjoying StSC! If you are getting popups please try clearing your browser cache.

Comment