-

-

This BATF connection is very revealing. Please notice the date for this process (linked below) and please allow for how much I have learned and changed over the years. There is something in it about the BATF owning the phone line for the US Supreme Court that has always struck a chord - chiefly with your point in post.Originally posted by fishnet View Post

Thank you.

Comment

-

Everybody loves to complain about taxes but wants the benefits they provide. Roads, schools and so on have to be paid for, at the federal, state and local levels. State income taxes have been a bit of a hot topic. These taxes are despised by some and several states are taking a look at ditching them, but there is evidence as to how good and bad they really are. Read more: State Income Taxes, Sales Taxes.Comment

-

Originally posted by mariusB View Post

Thank you Marius;

Overall my gripe is not about taxes, it is about central banking and United Nations municipal combinatoric mathematics. Simply put, that debt has been assigned value and more specifically beyond the creditor, in marketplaces created out of conditioned delirium called Bailout, Derivatives and now Quantitative Easing. That value is cancelled in any new suitor going through the Lesson Plan described here:

1) true identity

2) record forming

3) redeeming lawful money

As I say quite often though, this is not for everybody - the brain trust anyway. We manage a carefully regulated relief valve system for a highly compressed information infrastructure called Money. If everybody suddenly realized how absurd it is to assign value to debt (Special Drawing Rights) then the world's economies would all disappear overnight.

Comment

-

Roads are paid by gasoline taxes, schools are paid by property taxes. Income taxes, according to the Grace Commission report cover letter are used to pay the interest on the US Debt and to transfer payments [social security, welfare, etc.] http://docs.law.gwu.edu/facweb/jsieg...taxes/debt.htm The only reason income taxes are still in place is to attempt to soak the buying power out of the pockets of the people to keep the sham of a monetary system afloat for as long as possible.Originally posted by mariusB View PostComment

-

The following seems quite relevant or in parallel:Originally posted by David Merrill View Post

Topic 431 - Canceled DebtTaxable or Not?

A debt includes any indebtedness whether you are personally liable or liable only to the extent of the property securing the debt. Cancellation of all or part of a debt that is secured by property may occur because of a foreclosure, a repossession, a voluntary return of the property to the lender, abandonment of the property, or a principal residence loan modification.

In general, if you are liable for a debt that is canceled, forgiven, or discharged, you will receive a Form 1099-C (PDF), Cancellation of Debt, and must include the canceled amount in gross income unless you meet an exclusion or exception. If you receive a Form 1099-C but the creditor is continuing to try to collect the debt, then the debt has not been cancelled and you do not have taxable cancellation of debt income.

You must report any taxable amount of a cancelled debt for which you are personally liable, as ordinary income from the cancellation of debt, on Form 1040 (PDF) or Form 1040NR (PDF) and associated schedules, as advised in Publication 4681 (PDF), Canceled Debts, Foreclosures, Repossessions, and Abandonments (for Individuals). You must report the taxable amount of a taxable debt whether or not you receive a Form 1099-C.

Caution: If your debt is secured by property and that property is taken by the lender in full or partial satisfaction of your debt, you are treated as having sold that property and may have a taxable gain or loss. The gain or loss on such a deemed sale of your property is an issue separate from whether any cancellation of debt income associated with that same property is includable in gross income. See Publication 544, Sales and Other Dispositions of Assets, and Publication 523, Selling Your Home for detailed information on reporting gain or loss from repossession, foreclosure or abandonment of property.

Canceled debts that meet the requirements for any of the following exceptions or exclusions are not taxable.

Canceled Debt that Qualifies for EXCEPTION to Inclusion in Gross Income:

Amounts specifically excluded from income by law such as gifts or bequests

Cancellation of certain qualified student loans

Canceled debt, that if paid by a cash basis taxpayer, would be deductible

A qualified purchase price reduction given by a seller

Any Pay-for-Performance Success Payments that reduce the principal balance of your home mortgage under the Home Affordable Modification Program

Canceled Debt that Qualifies for EXCLUSION from Gross Income:

Debt canceled in a Title 11 bankruptcy case

Debt canceled during insolvency

Cancellation of qualified farm indebtedness

Cancellation of qualified real property business indebtedness

Cancellation of qualified principal residence indebtedness

The exclusion for "qualified principal residence indebtedness" provides tax relief on canceled debt for many homeowners involved in the mortgage foreclosure crisis currently affecting much of the United States. The exclusion allows taxpayers to exclude up to $2,000,000 ($1,000,000 if married filing separately) of "qualified principal residence indebtedness."

Generally, if you exclude canceled debt from income under one of the exclusions listed above, you must reduce your positive tax attributes (certain credits, losses, basis of assets, etc.), within limits, by the amount excluded. You must file Form 982 (PDF), Reduction of Tax Attributes Due to Discharge of Indebtedness (and Section 1082 Basis Adjustment), to report the amount qualifying for exclusion and any corresponding reduction of certain tax attributes.

If you received a Form 1099-C and the information is incorrect, contact the lender to make corrections. Refer to Publication 4681 (PDF), Canceled Debts, Foreclosures, Repossessions, and Abandonments (for Individuals), for more detailed information regarding taxability of canceled debt, how to report it, and related exceptions and exclusions. Additional information can also be found in Publication 525, Taxable and Nontaxable Income. If you received a Form 1099-A (PDF), Acquisition or Abandonment of Secured Property, review Topic 160 for additional information. [Source: IRS.]

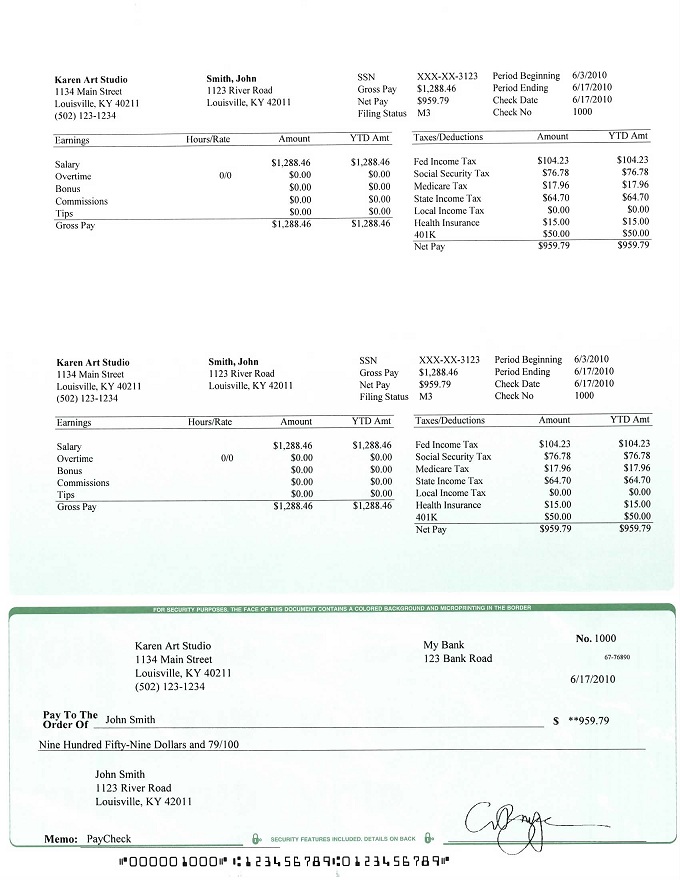

Notice the "Bank's position" on the payroll checks vs. on a personal check (below).

Perhaps the significance is in whether you discharge or someone else does?payment (Act of paying), noun acquittal, acquittance, amortization, amortizement, clearance, compensation, defrayment, disbursement, discharge of a debt, liquidation, outlay, quittance, receipt in full, recompense, reimbursement, remittance, restitution, return, satisfaction, settlement, spending, subsidy

Last edited by allodial; 10-01-13, 06:43 AM.All rights reserved. Without prejudice. No liability assumed. No value assured.

Last edited by allodial; 10-01-13, 06:43 AM.All rights reserved. Without prejudice. No liability assumed. No value assured.

"The object in life is not to be on the side of the majority, but to escape finding oneself in the ranks of the insane." -- Marcus Aurelius"It is the glory of God to conceal a thing: but the honour of kings is to search out a matter." Proverbs 25:2Prove all things; hold fast that which is good. Thess. 5:21.Comment

-

It is articles like this that shows you that you are not the owner of your land and your just a tenent of the property if you don't pay the tax to live on it.Originally posted by Goldi View Post

So then who owns the land?

Treasurer John Petalas said the Internet-driven sale collected that from 1,360 parcels from among a total of 9,000 properties whose owners failed to pay overdue taxes and special assessments. It also represents a bidding frenzy on a smaller amount of commercial sites. He said one property where the tax debt was $14,762 was sold at auction for more than $280,000, and a second property with an $81,000 tax debt sold for $541,000.

Petalas said the $21.6 million figure includes $4.7 million in taxes and late penalties county, municipal and township government officials can keep

(that must be nice, keep and do what with it).

The remaining $16.8 million is the surplus value that will be paid either to the delinquent owners who lost their properties or back to the buyer with a small profit if the owner redeems the property by paying 10 percent of the successful bid.

Petalas credited the success of the online auction conducted by SRI, Indianapolis-based auctioneer, which received bids around the clock from people across the country.

"And if I could I surely would Stand on the rock that Moses stood"Comment

-

[QUOTE=Chex;11756]It is articles like this that shows you that you are not the owner of your land and your just a tenent of the property if you don't pay the tax to live on it.

So then who owns the land? [QUOTE]

When a property is mortgaged, the singular title on it, the land patent, has to be shelved so the title can be split. The legal title then goes to the occupant of the home, the "owner" and the equitable title is then available to be held by the county assessor/treasurer. When foreclosed, the bank gets the legal title to convey. Who gets the benefit of the profits, fees, rents, surpluses of investing the "res"? The equitable owner. Who pays the fees, fines, taxes? The legal owner. Isn't that what is going on with property taxes? The counties MUST hold an interest in the property to be able to bond it up. That's how they are doing it.Comment

-

Interesting, thanks for that piece Goldi.Originally posted by Goldi View Post

Title is a legal term for a bundle of rights in a piece of property in which a party may own either a legal interest or equitable interest.

The rights in the bundle may be separated and held by different parties. [That would be the township and you the owner.]

It may also refer to a formal document such as a deed that serves as evidence of ownership.

Conveyance of the document may be required in order to transfer ownership in the property to another person.

Title is distinct from possession, a right that often accompanies ownership but is not necessarily sufficient to prove it.

In many cases, both possession and title may be transferred independently of each other.

For real property, land registration and recording provide public notice of ownership information.

In United States real estate law, typically evidence of title is established through title reports written up by title insurance companies, which show the history of title (property abstract and chain of title) as determined by the recorded public record deeds;

[1] the title report will also show applicable encumbrances such as easements, liens, or covenants.

[2] In exchange for insurance premiums, the title insurance company conducts a title search through public records and provides assurance of good title, reimbursing the insured if a dispute over the title arises.

[3] In the case of vehicle ownership, a simple vehicle title document may be issued by a governmental agency.

At common law equitable title is the right to obtain full ownership of property, where another maintains legal title to the property.

[4] Legal title is actual ownership of the property. When a contract for the sale of land is executed, equitable title passes to the buyer.

When the conditions on the sale contract have been met, legal title passes to the buyer in what is known as closing.

Legal and equitable title also arises in trust.

In a trust, one person may own the legal title, such as the trustees.

Another may own the equitable title such as the beneficiary.

So there must be a contract describing the terms and conditions when we purchase a building on a piece of property belonging to property abstract and chain of title owner.Last edited by Chex; 10-03-13, 01:08 AM."And if I could I surely would Stand on the rock that Moses stood"Comment

-

Tenancy in Common http://www.osbar.org/_docs/public/lioa/chapter6.pdf(Common paperwork)Originally posted by Chex View Post"And if I could I surely would Stand on the rock that Moses stood"Comment

-

Historically, when property was mortgaged, the title was transferred to the creditor. After complete settlement of the terms of the mortgage, the title was re-conveyed or redeemed by the debtor.Originally posted by Goldi View Post

Historically, the letters patent was issued by the king. This patent was not absolute ownership or dominion. A letters patent is still qualified ownership for their would be terms and conditions written into the patent for the benefit of the king.

I will agree that there is some interest which the county purports to have in the land and appurtenances thereon.Originally posted by Goldi

The tenant, in most instances, will have legal and equitable interest in the property. There is some liability attached to the legal title upon tenure of such.

With registration and mortgage, the property is treated as a registered investment.Originally posted by Goldi

The presumption being that one is in commerce for profit and gain.

Perhaps the counties purport to hold an interest, but no one bothers to research the law and challenge them on such claim?Originally posted by Goldi

Comment

-

All deeds are color of title.Originally posted by Chex View Post

The original deed or first title deed is the land patent or land grant.

Deeds color who the holder of the patent or grant is for the patent or grant shall be as is without modification.Comment

-

In Massachusetts, things are different in name but not in form. A "warranty deed" says that the seller will warrant and defend the buyer's title against adverse claims by others; but since most sellers do not want to, effectively insure the title on behalf of the buyer, most people use a "quitclaim deed", which in contrast to the use of those words in other states means that the seller will warrant and defend the title ONLY against issues which arose when she or he actually held title. This is exactly like the "special warranty" deed mentioned by shikamaru.

The "bargain and sale" deed and "quitclaim deed" mentioned by shikamaru are called a "release deed" or a "deed without covenants" in Massachusetts. Since, in the normal course of business, no buyer of real estate would ever, in their right mind, accept such a deed, you will only see this kind of deed in a tax sale or foreclosure sale by a governmental entity or a foreclosing mortgagee. In this case, it is solely up to the buyer to review the title for at least the previous 50 years to see if any encumbrances or other title issues exist.

I bought my house 30 years ago this month, using a quitclaim deed to my wife and I as tenants by the entirety. Just for fun, I ran the title as far back as I could, and got to 1688 before the trail ran dry. It turned out that the woman who sold the land then was the daughter and heir of a man who came over with the original 1630 Puritans, and who was given fee simple title to his land by the Crown.Comment

-

Small correction: Chex enumerated the list of varying types of deeds.Originally posted by bobbinville View PostComment

-

Thanks! My aging eyes passed right over that....Comment

- If this is your first visit, be sure to check out the FAQ by clicking the link above. You may have to register before you can post: click the register link above to proceed. To start viewing messages, select the forum that you want to visit from the selection below. If you would like to post in these forums please send a PM directly to David Merrill.

- All transactions on PayPal and elsewhere are demanded to be redeemed in lawful money as found in Section 16 of the Fed Act and at Title 12 USC 411.

- Thank you so much for enjoying StSC! If you are getting popups please try clearing your browser cache.

Comment